The idea that crashes can be reasonably accurately charted and forecast based upon historic models of crashes sounds outlandish. There’s several knee-jerk reactions as to why this should not be possible. In this post we’re going to look at some of the common ones and relate them to real examples to test them.

The Fed in the market makes market’s different now.

When we’re talking about broad index market risk it would seem unwise to use models from the early 1900’s in today’s market. The Fed playing such a big role in the market would make any of these models from previous times redundant, one would assume.

Here’s a video from 2008. The great crash is late into development and this video is covering the differences between the monetary policy of 1920 (When there was a similar crash) and the current monetary policy of the day (As you probably know, the birth of the “Brrr”).

In the video the speaker goes through the differences. How in the wake of the 1920’s crash there was no Fed in the market (The Fed did nothing in the market until 1922) and the President would persistently promote deflationary measures. Juxtaposed against 2008, which was a Fed inflation based recovery.

Here’s what the crashes look like in the charts.

Which one the inflationary and the deflationary based recoveries? In which one was it the Fed that upped the market? The two charts are effectively interchangeable.

Here they are with the time and price added in.

Key things here;

Pullback around 161.

Hits 220 and pullback.

Market goes into strong uptrend over 261.

Key things here;

Pullback around 161.

Hits 220 and pullback.

Market goes into strong uptrend over 261.

Both moves take around about 40 bars to reach the high.

These recoveries are significantly similar. If in 2008 heading into 2009 you’d used a model of the recovery from the 1920’s crash, you’d have had more actionable insight into what would become the future real market swings that any/most other forms of analysis would have offered you.

The real world conditions at the time could not have been further apart, but the real charting moves really could not have been much more similar. The recovery swings match 1:1 during large parts of the move with only some slight deviations. Highly improbable in a random walk market.

Markets Move on News

Since most market crashes occur as the direct result of sudden shock news events (Often then building upon themselves and bringing in the Reflexivity effect) it would be reasonable to assume there should be no obvious foreseeable technical warnings of a crash coming. Charts can not foresee news events.

Yet, through the ages markets have boomed and crashed and while there have been a host of different real world reasons for this the ways in which the price moves actually formed has been remarkably similar ways. The same types of methods would have been effective in picking out highs and lows regardless of the news.

The 1917 crash in the DJI would happen mainly through the period of America being involved in World War One. The steep part of the crash would begin as the US entered the war and the crash would abruptly end when the war was declared over in 1918. On the face of it, this crash was fully dictated by the war.

However, the move also started after the market has ranged, made a false crash and then made a strong 161 extension of this range. The 161 extension would accurately forecast the price at which the DJI would make its high before the crash began. It would do this before the news was foreseeable.

If once the top was in a fib was drawn from the low to the high of this last swing up in the DJI, the down move would end on the 161 extension of this move. Matching up perfectly with the new news events, but a signal that could be generated long before the fact. As soon as the market made its first break.

One may well pass this off as chance or the finding of patterns because they are being looked for, but if someone was aware of these concepts they’d have seen the exact same things repeating in the March 2020 Covid crash in the SPX. The market would trade 161 high to 161 low - through a flurry of news events.

These 161 entry and exit levels would catch over 80% of the March 2020 crash. The signals forming even before the earliest news of the virus coming out China.

Isolated Patterns Can Not be Overall Useful

These are specific things in isolated crashes. Being able to suggest some efficacy in an idea based upon small sample sizes is easy but can be misleading. The finding of things looked for, rather than discovery of things that were always there. Can these commonalities be found over longer periods of time?

To address this we’ll flip back to my two favourite crashes that very few people know about. The 1915 and 1920 bear markets. A footnote in history now, but the 1920 crash was for a time known as the “Great Depression”. You’ll be able to find it now labelled as the “Forgotten Depression”.

This was a different market and a different time. There was no Fed in the market. Deflationary measures were promoted. Markets worked on Open outcry, not on apps. Prices were read from the ticker tape. In all obvious ways, it was a totally different world to the modern world.

But the overall price swings created in the market were notable similar to those of the crashes of 2000 and 2008 in the DJI.

We could go deeper into the ratios of different swings here and point out various matching points, but we’ll prevent getting into too many dry and technical details at this point. Instead we’ll just do a thought experiment of what would have happened if you used the 1920 crash action to forecast 2009+ action.

As covered previously in the post, this would have been very effective in the recovery to the high. It ran close to swing to swing and it took about the same amount of candles to do it. Let’s look at the the move out of the 1920 low a bit closer to see what sort of forecast it would have generated.

The most obvious thing we can see out of the 1920 low is the change in the angle of the trend. Coming from a trendline somewhere close to the 10 degrees slope and heading into a much sharper trendline of over 40 degrees slope. During this time the public came into the market - inline with the Minsk model.

{kind=link}

The increase of a trend angle from around 10 degrees to 40 degrees would have been a very good working model to take into the 2009+ rally. You would have expected the trend to take on a stronger upward momentum and you may well have expected the markets to become a lot more publicly popular.

The rally of the 1920’s would give way to the Great Depression. If a fib was drawn from the low to the high of the first rally and crash, the top of the Great Depression came in just over the 423 extension of this swing. It would have accurately forecast the area of most bearish risk.

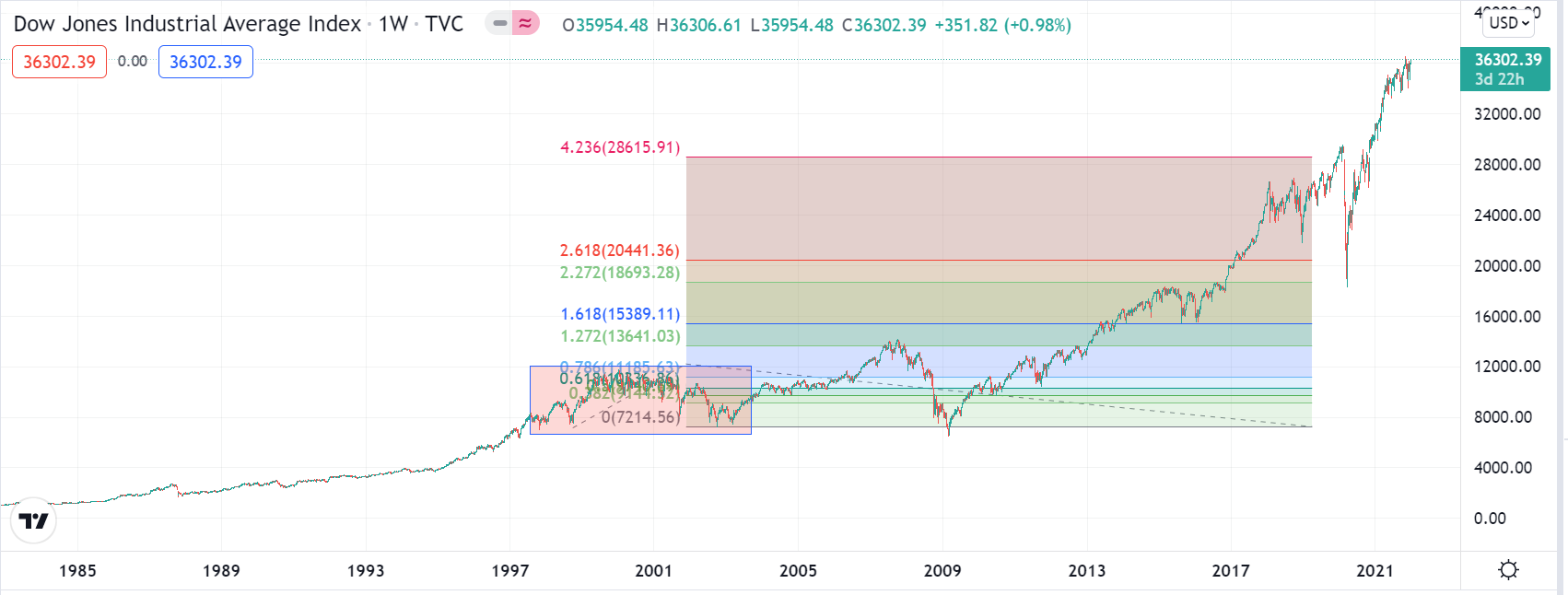

If we apply the same rules to DJI of modern times, we can see it hit this 423 extension early in 2020 and this was the price where the high of the Covid crash would be made.

This was an area someone could know to watch for being important far ahead of time. Long before even the early signs of weakness in the 2018 drop. The long term resistance level of the 423 coupled with the short-term entry signal of the 161 top were the two main signals used to generate this Feb 2020 forecast.

This forecast was accurate in the drop section of the move but inaccurate in the forecast of there being no new high (More on that later).

So, working with the 1915 - 1929 price action as an approximate guide for the market action after the 2000 Dot.com crash the following useful forecasts could have been generated;

After a drop of close to 50%, market will rally to new high.

On a spike high the market will drop around 50%.

It will take about 40 candles to recover to the high.

The steepness of the trend will increase four-fold.

Big take profit area is generated on 423 extension.

Given the nature of the Minsk model, one would probably not bet against the saying, “To the moon” being a lot more popular after the angle increase and 423 extension.

While it can not be said with any degree of certainty what the future will hold, it’s very fair to say that making these observations ten years ago would have helped to create a significant edge in the market. Understanding zones to accumulate and zones to take profit into.

The only notable difference in the rally and following bear market of the 1920’s and the post-2008 rally is the depth of the fall. The crash starting in 1929 would continue until it has traded all the way under the lows of the start of the Roaring 20’s boom. Heavily punishing those entering late in the cycle.

The move this would have implied in the DJI in 2020 did not come to pass. In a duplication of the model the rally would have truncated before making a new high and then a strong and sustained bear market would have taken grip, driving us down to under the lows of 2008.

But was that it? An optimist can hope so. A pessimist can fear not. The pragmatist knows it’s best to prepare for all the possible outcomes.

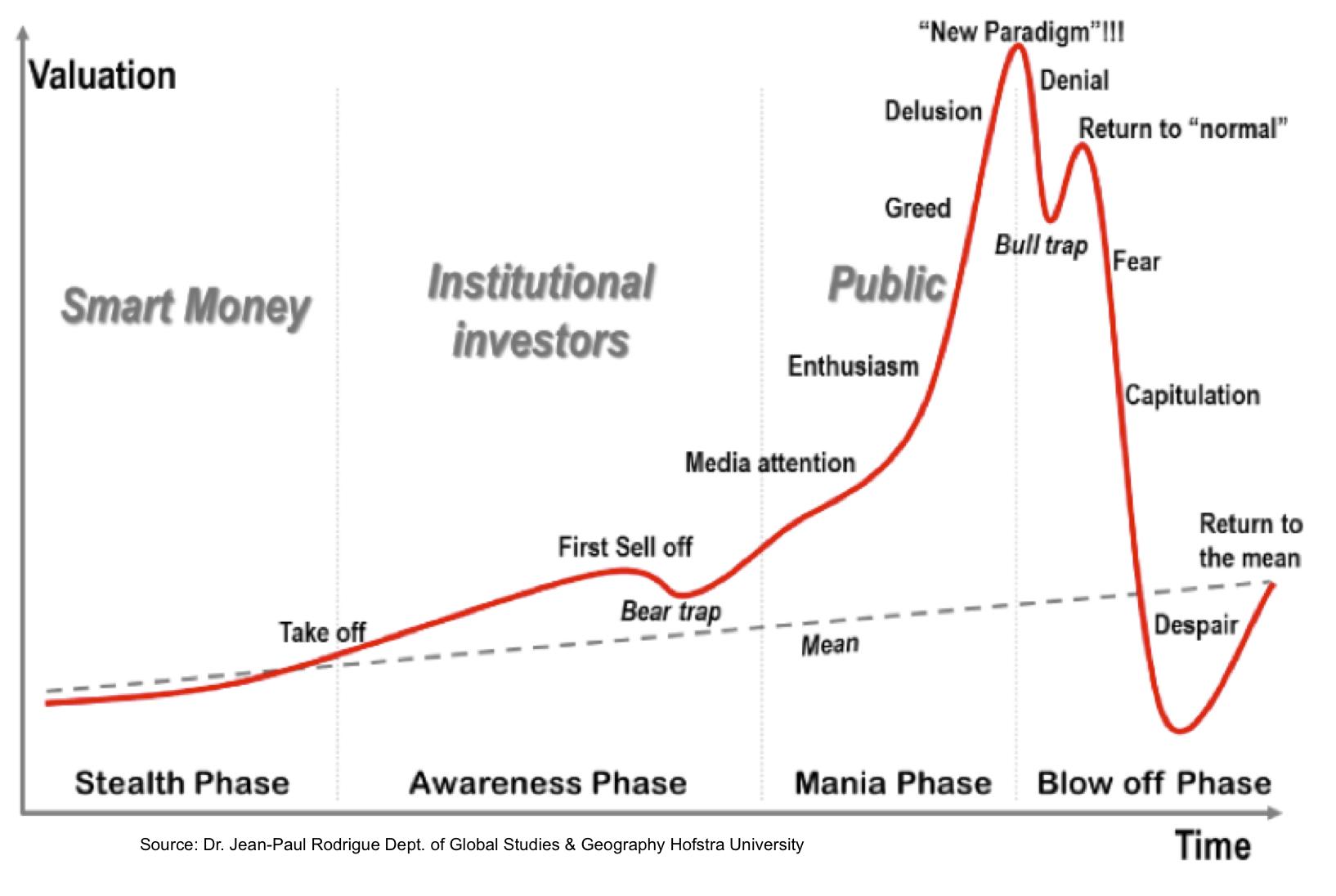

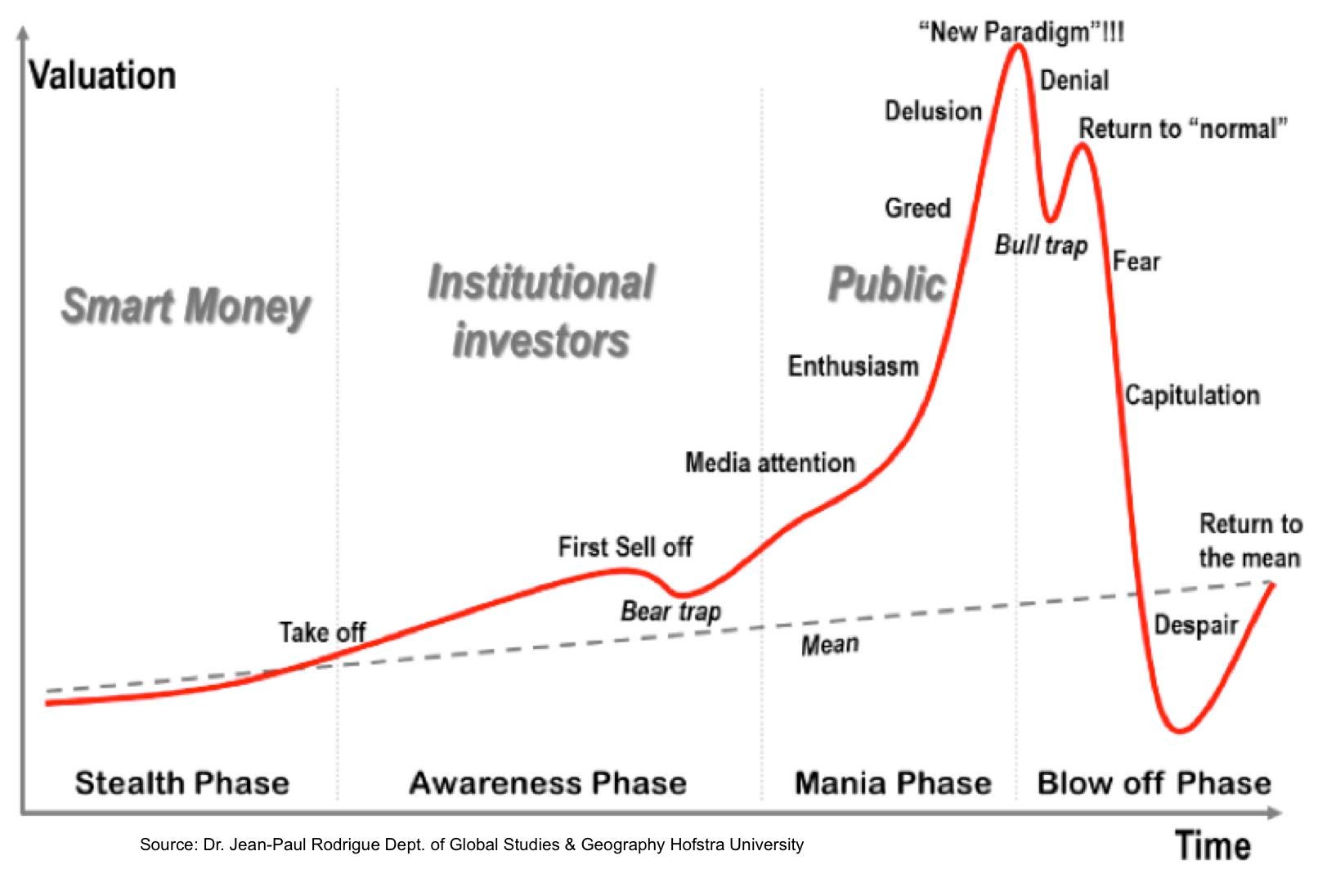

The question is, and the time to ask is now, has the Minsk model failed? Did the “Return to Normal” section of the bull trap break and is the risk of a major crash revering prices to the mean now over? Is it a brave new world? Or it is just the same old trap? Are we witnessing the illusion of the “New Paradigm”?

The body of work presented here is intended to put together actionable trading and hedging plans that would help to mitigate risk of ruin (Or be very profitable, for a speculator) in the event of the market having anything up to and including this style of major crash.

The recovery from the 1929 crash would take 24 years to get back to the high. During this time there’d be markets that went sideways for a decade. This is not a trivial risk. It’s firmly my belief when people talk about “Being in it for the long-term” they discount the risk of this type of event happening in their lifetime.